Historical Context

In 1869, the United States had no securities regulator, no central bank, and no mechanism to prevent individual speculators from manipulating national markets. The telegraph — the era's dominant communications technology — gave information to those who controlled it and nothing to those who didn't. On September 24, that asymmetry destroyed thousands of ordinary Americans in a single morning.

Friday morning, September 24, 1869. The Gold Exchange on New Street, Manhattan. Thomas Kellerman stood on the trading floor, his collar already soaked with sweat though the morning was cool. He had been a messenger boy six weeks earlier. Then he had borrowed money. Fifty dollars. He had taken it to a broker with a name he'd heard whispered in corners: buy gold. Hold it. The price is going up.

By September 20, Thomas Kellerman had been worth $8,000. He had not slept well since.

The price of gold that morning was $162 per ounce — the highest in American history. It had been rising for months, climbing higher and higher, defying every principle of economy. The federal government said it didn't make sense. The newspapers said it didn't make sense. But the gold kept rising, and men like Thomas Kellerman — men with nothing, suddenly men with everything — kept buying, kept holding, kept believing that someone, somewhere, knew something they didn't.

At 10:02 AM, the bell rang again.

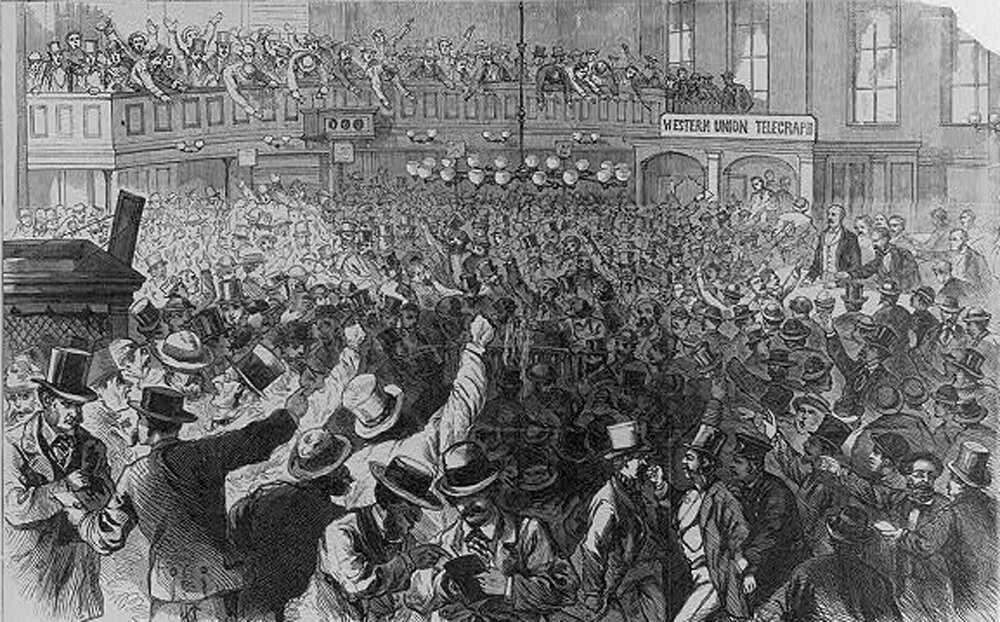

The first wave of sales hit the floor like a wave breaking against stone. Gold dropped from $162 to $160. Then $158. Within seconds, it was falling faster than the price could be written down. Men began to shout. The shouting became screaming. Within minutes, gold had fallen to $140. Within the hour, it had collapsed to $130 — the lowest price in weeks.

Thomas Kellerman watched his $8,000 evaporate into air. Within the hour, it was gone. Within two hours, his fifty-dollar loan had cost him money he would never have earned in ten years of messenger work. He was not alone. Thousands of men — clerks, merchant sons, widows who had hidden their savings, telegraph operators who thought they had finally understood the secret language of money — stood frozen in the chaos of the Gold Exchange, watching fortunes die in real time.

One man did not watch. One man had been waiting for this moment for weeks.

The Telegraph as a Weapon

Jay Gould was not the richest man in America, but he was the most dangerous. He was thin, bearded, with eyes that seemed to calculate the moment they looked at you. He had made his name in railroads — not by building them, but by understanding them, by reading the hidden mathematics of profit and vulnerability that other men missed. He was 33 years old in 1869, and he had already been rich and poor and rich again. He understood the difference between luck and method.

In the spring of 1869, Gould had become obsessed with gold.

The federal government held gold as the foundation of American currency. The more gold men controlled privately, the more leverage they had over the national money supply. It was a simple mathematical principle: if Gould and his partner James Fisk could buy enough gold to corner the market — to control the supply — they could name the price. They could force other men to buy gold from them at whatever price they demanded. And if the government tried to intervene, if the Treasury Department tried to release gold from its vaults to break the corner, Gould would know about it before the market did.

Because Gould controlled the telegraph.

A man who controlled the telegraph held a weapon invisible to the eye but absolute in its power.

The Western Union telegraph company was the internet of 1869. It was how information moved. It was how orders were placed. It was how prices were transmitted. A man who controlled the telegraph held a weapon invisible to the eye but absolute in its power. Gould did not officially own Western Union — but he had enough influence, enough stock, enough connections, that he could know what was happening in Treasury offices before Wall Street traders heard the news. He could transmit information to his brokers while his competitors were still in the dark.

He called it advantage. Congress would later call it something else.

Gould's plan was elegant in its simplicity: accumulate gold through the summer, create the appearance of scarcity, drive the price up through psychology and rumor, and then, when the price reached its peak, sell everything at once before the inevitable collapse. But there was a problem. The federal government had gold. If the Treasury released even a small amount, it would break the corner instantly.

So Gould had set out to prevent the Treasury from releasing gold.

His weapon was not money. It was family.

Abel Rathbone Corbin was Gould's brother-in-law, connected by marriage and by calculated courtship to President Ulysses S. Grant. Gould had convinced Corbin to buy gold alongside him — to become a partner in the scheme. Once Corbin was invested, once Corbin had money riding on the gold price, Corbin's ears would be pressed to Grant's office door. Corbin would whisper arguments into the President's ear: Don't release the gold. The economy needs the gold to stay high. Releasing gold would destabilize commerce.

By the summer of 1869, it was working. President Grant — convinced by his brother-in-law's arguments, or perhaps simply distracted by larger matters of state — had begun to resist calls from his own Treasury Secretary to release government gold and break the corner. The price climbed higher. Men who understood nothing about markets began to borrow money to buy gold. Clerks quit their jobs. Widows liquidated their savings. Thomas Kellerman, who had never owned anything but his own labor, borrowed $50 and suddenly had a claim on $8,000 of phantom wealth.

By mid-September, Gould had accumulated nearly $100 million in gold contracts. The entire scheme balanced on one premise: that the government would not intervene. That the Treasury would remain silent. That the door to the federal vaults would stay locked.

On September 18, President Grant finally understood what was happening.

The Morning When Everything Reversed

What Gould did not know was that Grant's patience had a limit. What Gould did not know was that people close to the President — Treasury Secretary Daniel Richardson, among others — had been warning Grant for weeks that a financial catastrophe was coming. What Gould did not know was that Grant had finally stopped listening to Abel Corbin and started listening to his own instincts.

On September 18, Grant sent a single instruction to the Treasury Department: release gold. Sell government gold at $130 per ounce. Flood the market. Break the corner.

The instruction was sent by telegraph — the same medium Gould had used as his instrument of power. But this time, Gould did not know it was coming. This time, the telegraph carried news he had no way to anticipate.

By the time Gould realized what was happening, the government had already authorized the release of $4 million in gold. The price had already begun to fall. Gould's $100 million in contracts — vast on paper, worthless in fact — were about to vaporize.

What happened on the morning of September 24 was not a market correction. It was a crater opening beneath the feet of every man who had believed that gold prices would rise forever.

By noon, the Gold Exchange was a scene of chaos that no contemporary account could adequately describe. The New York Times reported it with the precision of a disaster: men weeping openly, men trying to push past others to reach the exits, men standing motionless, staring at nothing, their minds unable to process the velocity of their own ruin. One man collapsed on the floor of the exchange and had to be carried out. Another — a respectable merchant — was found on a bench in City Hall Park an hour later, having drunk a bottle of laudanum.

Thomas Kellerman did not drink poison. He walked out of the Gold Exchange at 3 PM, when the bell rang to close the trading floor, having lost everything he had borrowed and everything he had imagined owning. He went back to being a messenger boy. He stayed in the boarding house. He lived his life with the knowledge that he had been, for six weeks, rich beyond measure, and that money was a word that meant nothing.

The numbers were staggering: estimates ranged from $10 million to $50 million in speculative losses. Entire firms had collapsed. Small investors had been wiped out. A network of secondary panics began to ripple through other markets — men who had speculated in gold now liquidating other holdings to cover their losses, a cascade of selling that threatened to collapse the entire financial system.

And one man sat in his office, reading telegrams, understanding that he had lost control of his own weapon.

The Reckoning

Jay Gould had not lost everything. He was too clever, too diversified, too careful for that. But he had lost the game, and the loss was public. Within days, he had begun a campaign of denial. The price manipulation, he claimed, was not his doing. He had simply been a trader. He had simply bought gold because he believed gold was undervalued. The fact that he had accumulated $100 million in gold contracts was irrelevant.

Congress did not believe him.

By December 1869, the House Judiciary Committee had announced an investigation into the Gold Panic. By the spring of 1870, hearings had begun. Gould was called to testify. So was Fisk. So was Grant himself — an embarrassing appearance in which the President had to explain, in public, that he had been manipulated by his own brother-in-law.

The testimonies were stunning. Gould's claim that he was merely trading was contradicted by his own actions — the accumulation of contracts far beyond any reasonable trading position, the campaign to prevent Treasury gold sales, the use of his telegraph network to gain information advantage over ordinary traders.

One moment from the testimony would echo through Congress for decades. A congressman asked Gould directly: "Did you know that thousands of ordinary citizens were buying gold based on rumors you spread? Did you know that widows were liquidating their savings? Did you know that messenger boys were borrowing money they couldn't repay?"

"I cannot be responsible for what others choose to do with their money."

Jay Gould, Congressional testimony, 1870

Congress decided that someone needed to be responsible. If individual traders could not be trusted, if telegraph operators could use information asymmetry as a weapon, if government officials could be manipulated by family connections, then the government itself needed to intervene. Not to prevent trading, but to make trading transparent. Not to forbid speculation, but to require that all traders operate on the same information at the same time.

The Telegraph Panic had exposed a truth that money men had preferred to ignore: financial markets required oversight, or they would become weapons.

The Institution Built from Ashes

The reforms that followed Black Friday 1869 were halting and insufficient. Congress passed rules requiring the Treasury to maintain a gold reserve and to sell gold transparently. New York State passed regulations requiring brokers to disclose their positions. These measures were weak, often ignored, frequently circumvented. But the principle was established: the government had the right to regulate how financial markets operated.

That principle would take six decades to fully mature. In 1933, after the stock market collapse of 1929 had wiped out millions of small investors — investing on margin, buying on rumors, trusting brokers who had their own financial interests in mind — Congress finally passed the Securities Act. In 1934, it established the Securities and Exchange Commission. The SEC was designed to do what Congress had called for after Black Friday but lacked the courage to fully enact: to require transparency, to prevent manipulation, to ensure that all market participants had access to the same information at the same time.

The SEC's first chairman, Joseph P. Kennedy, was famously asked why the President had appointed a man known for his own stock market manipulations to oversee the market. Kennedy's answer was direct: "It takes a thief to catch a thief." It was a line that would have made Jay Gould smile.

But there was a difference between Gould's world and Kennedy's. In Gould's world, market manipulation was simply clever trading. By Kennedy's time, it was illegal. The telegraph that Gould had used as his invisible weapon had been replaced by the telephone and the ticker tape — technologies that moved faster, that were harder to control, that required regulation simply to prevent chaos. And the regulatory framework had been built on the foundation of Black Friday, 1869.

Unregulated markets are not free markets. They are weapons waiting to be fired.

The locked library door of 1907 had forced America to build the Federal Reserve. The telegraph crash of 1869 had forced America to ask a different question: Who watches the watchmen? The answer, written into law over six decades, was: everyone. Together.

Jay Gould died in 1892, still rich, still controversial, still refusing to acknowledge that his method had been anything but legitimate trading. The telegraph networks he had manipulated are long gone, replaced by fiber optic cables and wireless signals. But the principle he had revealed — that unregulated access to information was a weapon — remains the foundation of every financial regulation since.

The price of gold on September 24, 1869, had fallen from $162 to $130 in hours. But the institutional price of that crash was much higher. It was measured in the decades of regulation that followed, in the agencies built to prevent the next Gould, in the transparent markets that made manipulation harder though never impossible. It was the price of learning, finally, that money — real money, built on trust and traded between millions of people — required rules written not by traders, but by the representatives of the public they had harmed.

Thomas Kellerman is a composite figure representing the documented class of small investors — clerks, messenger boys, and household savers — who lost money in the Black Friday panic. His specific circumstances are invented; the financial losses and social conditions described are drawn from congressional testimony and contemporary press accounts. All named figures (Gould, Fisk, Corbin, Grant, Richardson, Kennedy) and their actions are documented historically. Direct quotations are sourced from congressional transcripts or contemporaneous reporting. Sources: House Judiciary Committee Report on the Gold Panic of 1869 (GPO, 1870); New York Times archives, September–October 1869; Charles Francis Adams Jr. and Henry Adams, Chapters of Erie (1871); SEC Historical Archive.